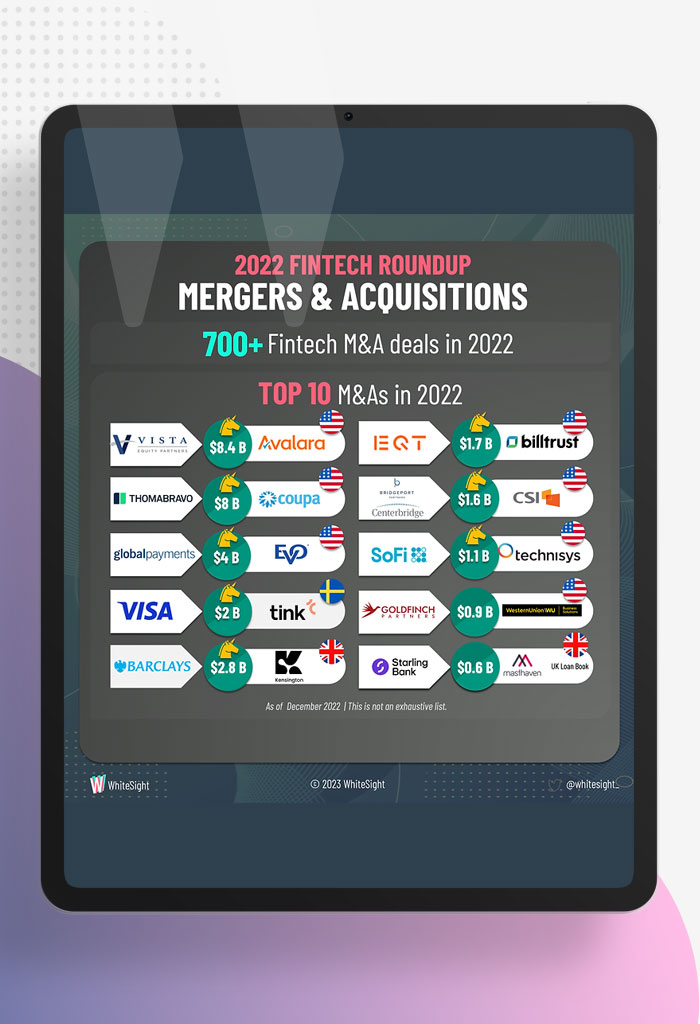

2022 FinTech M&A Roundup: Economic Climate Driving Industry Consolidation

2022 has been a year of two contrasting halves in the FinTech world. The first quarter of 2022, carrying the momentum from 2021, started with a bang with several Digital Banking and Digital Payments firms raising 100M+ funding rounds with eye-popping valuations. Since Q1 2022, FinTech valuations in both private and public markets have suffered a swift and massive correction over the last three quarters of 2022.

The FinTech industry has experienced a period of consolidation in 2022 due to the current economic climate, characterized by a slowdown and the prospect of a recession. This has led fintechs to seek mergers or acquisitions with other firms in order to unlock economies of scale and scope, as well as gain access to additional capital and other resources.

Consolidation is also being driven by the need for financial institutions to innovate and stay ahead of the curve by acquiring innovative fintechs and their tech capabilities and business expertise.

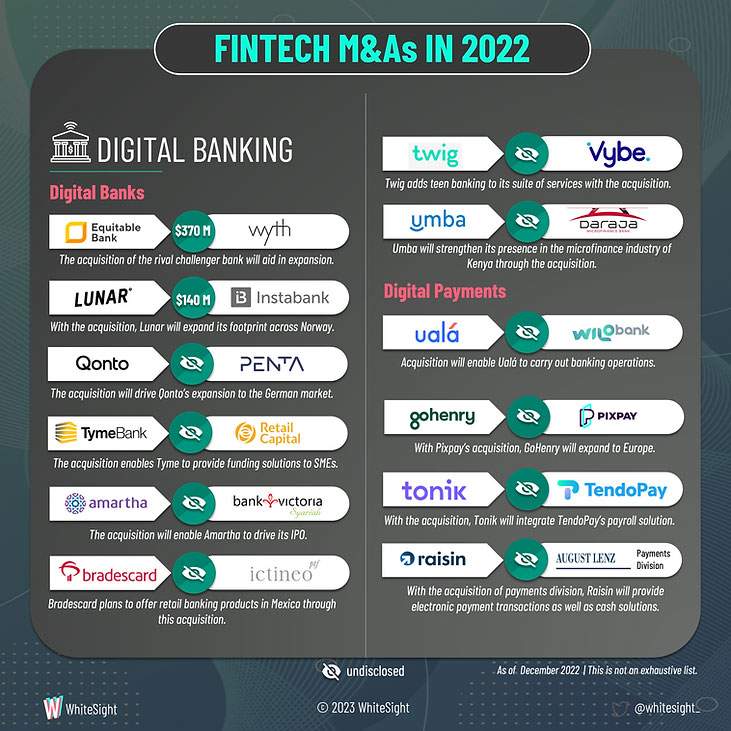

FinTech Mergers and Acquisitions Roundup 2022 provides a summary of notable M&As across the segments of digital banking, digital payments, FinTech infrastructure, embedded finance, and more.